Performance Materials

| Performance Materials key data | ||||||

|---|---|---|---|---|---|---|

| 4th quarter 2024 | 4th quarter 2025 | Change | 2024 | 2025 | Change | |

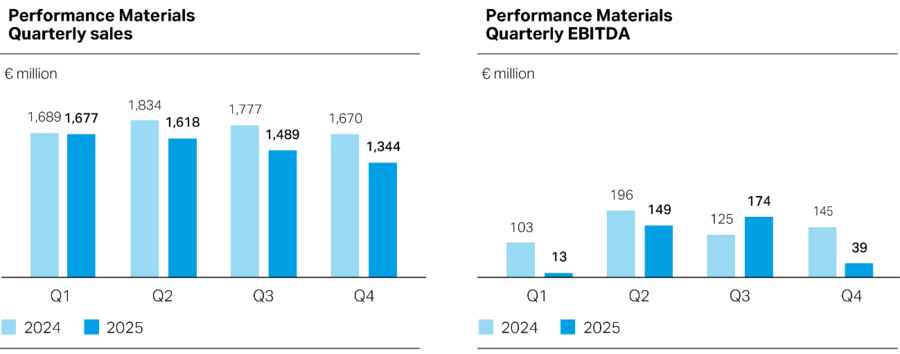

| Sales (external) | €1,670 million | €1,344 million | –19.5% | €6,970 million | €6,128 million | –12.1% |

| Intersegment sales | €510 million | €432 million | –15.3% | €2,228 million | €1,987 million | –10.8% |

| Sales (total) | €2,180 million | €1,776 million | –18.5% | €9,198 million | €8,115 million | –11.8% |

| Change in sales (external) | ||||||

| Volume | 5.6% | –4.6% | 11.9% | –2.9% | ||

| Price | –0.1% | –10.9% | –9.6% | –6.7% | ||

| Currency | –0.3% | –4.0% | –0.9% | –2.5% | ||

| Sales by region (external) | ||||||

| EMLA | €739 million | €521 million | –29.5% | €3,102 million | €2,568 million | –17.2% |

| NA | €400 million | €374 million | –6.5% | €1,720 million | €1,693 million | –1.6% |

| APAC | €531 million | €449 million | –15.4% | €2,148 million | €1,867 million | –13.1% |

| EBITDA1 | €145 million | €39 million | –73.1% | €569 million | €375 million | –34.1% |

| EBIT1 | (€55 million) | (€301 million) | 447.3% | (€42 million) | (€416 million) | 890.5% |

| Cash flows from operating activities | €355 million | €260 million | –26.8% | €574 million | €392 million | –31.7% |

| Cash outflows for additions to property, plant, equipment and intangible assets | €226 million | €136 million | –39.8% | €496 million | €496 million | 0.0% |

| Free operating cash flow | €129 million | €124 million | –3.9% | €78 million | (€104 million) | . |

1 EBITDA and EBIT include the effect on earnings of intersegment sales.

Sales in the Performance Materials segment were down 12.1% to €6,128 million in fiscal 2025 (previous year: €6,970 million). The drop was primarily driven by a 6.7% decline in average selling prices due to oversupply in the market, which coincided with lower raw material prices being passed on to customers. In addition, a 2.9% decline in volumes sold as well as adverse changes in exchange rates of 2.5% had a negative effect on sales.

In the EMLA region, sales dropped by 17.2% to €2,568 million (previous year: €3,102 million). This was caused mainly by a decline in the selling price level and in volumes sold, due, among other things, to an outage-related drop in plant availability, both of which had a significant adverse impact on sales. In contrast, exchange rate movements had a slightly beneficial effect on sales. The NA region’s sales decreased 1.6% to €1,693 million (previous year: €1,720 million), due especially to adverse exchange rate movements, which had a significant reducing effect on sales. Slightly lower average selling prices had an additional negative effect on sales. These factors were largely offset by a significant rise in volumes sold. Sales in the APAC region declined by 13.1% to €1,867 million (previous year: €2,148 million), driven by a significant drop in the selling price level. Additionally, adverse changes in exchange rates and lower volumes sold both had a slightly negative impact on sales.

EBITDA in the Performance Materials segment fell by 34.1% over the prior year to €375 million (previous year: €569 million). This was primarily driven by a drop in margins, as lower raw material prices were unable to fully offset the decrease in selling prices, and higher expenses of €111 million were incurred to implement the STRONG transformation program. The latter amount was mostly attributable to the closure of the joint venture production facility at the Maasvlakte (Netherlands) site. Moreover, a €43 million year-on-year drop in government subsidies to compensate for electricity prices attributable to the segment and adverse exchange rate movements had a reducing effect on earnings. This was set against a decline in fixed costs and lower provisions for short-term variable compensation, which boosted earnings. While sales volumes were down overall, the reduction of business with negative margins had a beneficial volume effect on EBITDA. In addition, the recognition – with a neutral effect at the Group level – of insurance compensation of €75 million due to the production stoppage in Dormagen (Germany) had a beneficial effect on earnings. This was set against insurance compensation of €55 million in the previous year. In addition, a year-on-year rise in gains on the sale of intangible assets in an amount of €20 million had a positive impact on earnings.

EBIT amounted to €–416 million (previous year: €–42 million), driven primarily by the decline in EBITDA and by a rise in impairment losses to €221 million (previous year: €63 million).

Free operating cash flow stood at €–104 million (previous year: €78 million), mainly because EBITDA was down on the previous year.